Non-major banks roundtable reveals how sector thrived despite challenges

It’s hard to believe a year has passed since the Reserve Bank of Australia increased the official cash rate for the first time in almost 12 years.

Lifting the cash rate 25 basis points from 0.10% to 0.35% in May 2022, the RBA board said it was the right time to begin withdrawing some of the “extraordinary monetary support” that had helped the economy during the pandemic. It also said inflation had risen more quickly than expected.

While economists have argued that the RBA took far too long to lift interest rates, the OCR now sits 3.85%, following 11 rate hikes. The board paused in April, but raised the cash rate again in May due to inflation.

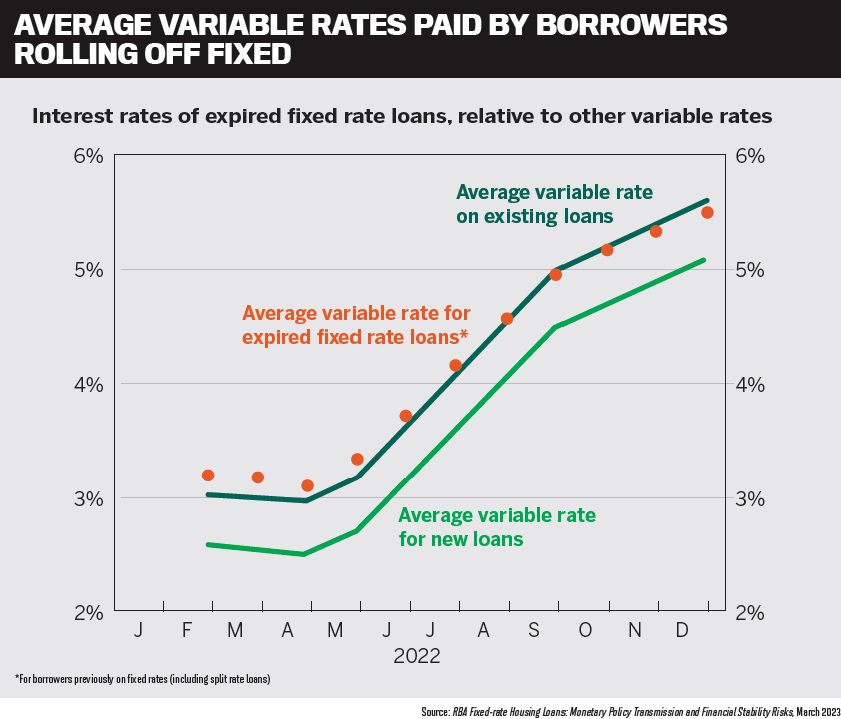

The days of record-low interest rates for mortgage holders seem like a long-distant memory. Variable rate borrowers are now being charged interest rates of at least 5% or more.

The economy is struggling to shrug off high inflation, labour shortages and supply chain problems. Higher interest rates are putting pressure on household budgets, and while many borrowers are well ahead on their mortgage repayments, there’s no doubt others are struggling.

Terms such as ‘mortgage prisoners’, ‘loyalty tax’ and ‘fixed rate cliff ’ have become commonplace in the mortgage industry. Refinancing queries have skyrocketed as customers flock to brokers to help them find better deals on their home loans. They include more than 800,000 people due to roll off their fixed rate loans over the next year.

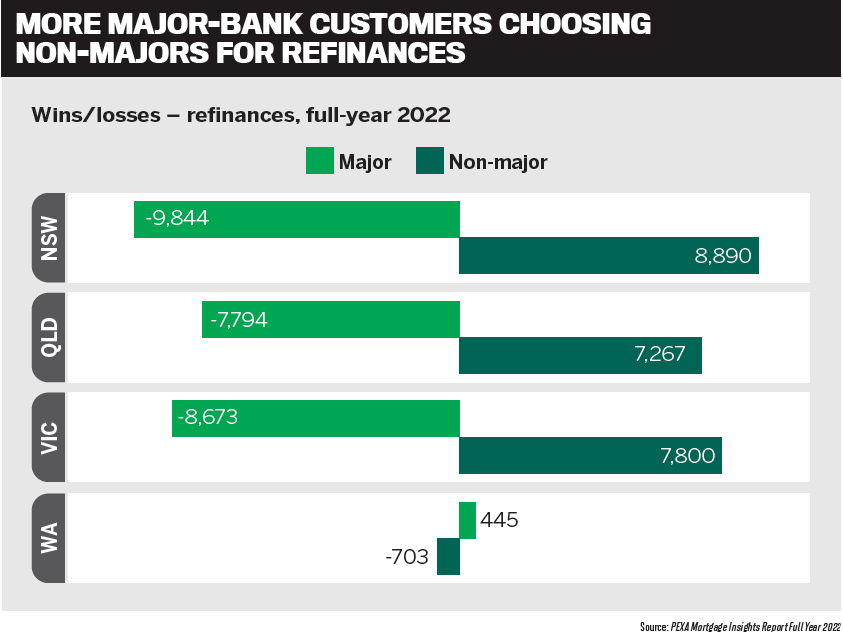

But in the midst of a tough economic period and intense mortgage competition, non-major banks have performed remarkably well. The PEXA Mortgage Insights Report for full year 2022 showed that major bank customers continued to refinance with non-major banks in the eastern states throughout the year.

Non-major banks also made up half of the top 10 banks in MPA’s Brokers on Banks 2023. MPA gathered the third party heads of some of Australia’s leading non-major banks to take part in its annual roundtable at Silks restaurant in Sydney. They included Glenn Gibson, head of sales and distribution at ING Australia; Ian Rakhit, general manager third party at Bankwest; Troy Fedder, head of broker partnerships at Suncorp Bank; and Simon Elwig, head of broker operations at BOQ Group (BOQ, ME Bank and Virgin Money Australia). They were joined by two figures in the mortgage broking industry, Melanie Cunliffe, owner of Indigo Finance, and Stephen Harris, general manager at Nectar Mortgages.

The discussion covered how the non-majors focus on strong relationships with brokers; the importance of balancing existing customer needs with the push for new customers; the role of cashbacks; technological improvements; post-settlement processes; and Revenue NSW’s decision to seek payroll tax from broker aggregators.

Q: How have non-major banks fared over the last 12 months in an era of rising interest rates and cost of living and inflation pressures?

Economic uncertainty and the changing interest rate environment have certainly challenged many Australians, said ING’s Glenn Gibson (pictured above). “I think both from a bank and broker perspective, everybody’s had to pivot to give that support to their customers to say, ‘OK, this is what it means, this is how your bank can help you, these are the steps you can take, and this is what your options are to get you through these challenging times’.”

Ian Rahkit said, “A point of difference for Bankwest has always been our genuine focus on delivering the best possible experience for customers, especially during challenging economic conditions. As part of that commitment to customers, we’re starting to look at various scenarios and segments to ensure we’re providing the right type of support to the right customers, because at the end of the day, delivering a positive experience is not only good for the customer but it helps Bankwest retain those valued customers.”

Rakhit (pictured above) said he was interested in brokers’ views on the customer sectors in which affordability might start to become a challenge.

“We’re starting to see more of that emotionally charged commentary again, such as ‘mortgage prisoner’,” he added.

Bankwest is looking at what it can do not only for its entire customer book but also for those who might need different types of help, ensuring it has support options available that can be tailored to a customer’s unique circumstances.

Rakhit remains confident in the strength of Bankwest’s book. He said the financial institution was proactively working with customers – particularly those approaching the end of fixed rate terms – to ensure they were in the best possible position to manage the changing economic environment.

“That’s why we look at a holistic picture of a customer, because a simple rate adjustment isn’t a silver bullet in an environment that experienced 10 consecutive rate rises before a pause, which is why our support response needs to be broader.”

Rakhit said that while the last few years had been good for non-major banks, he was more worried about the next 12 to 24 months. “Picking up on Glenn’s point, I think an increasing number of customers are going to start more acutely feeling the cost of living strain very soon.”

He said other indicators were useful, such as the amount of savings customers were holding in offset accounts and how far ahead they were on their mortgage payments, with both suggesting that Bankwest customers were, on average, in strong financial positions. “We know that at the beginning of rate rises, more than 95% of our home loan customers were more than three years ahead on their mortgage repayments, and that was a result of the very low interest rate period that preceded the current environment, and the impact COVID had on savings growth.

“Those home loan buffers and savings volumes are gradually reducing but not at a rate that indicates distress,” Rakhit said. “Instead, it’s reflective of cost of living increases and that customers are using those buffers to maintain their positive financial positions.”

Gibson said anybody who had a mortgage prior to the GFC had a built up a buffer, but customers who had taken out a mortgage in the last 12 to 18 months didn’t have that

Troy Fedder (pictured above) of Suncorp Bank said the broader financial services industry had faced some challenges in the past 12 months.

“As we look forward to the next 12 months there will be further challenges and opportunities to work through,” he said.

“The thing that really strikes me is just how critical brokers have been in the customer relationship. The value of brokers has never been higher.”

Fedder said the supporting role brokers had played in talking to their existing customers and being proactive was clear.

“From a non-major bank perspective, and certainly from Suncorp Bank’s point of view, I’d reflect on the last 12 months by saying there’s been really good progress and momentum for most of the non-major banks, as both brokers and customers look for brands that they trust and brands that will look after their customers.”

Simon Elwig (pictured above) said BOQ, ME Bank and Virgin Money Australia had been “investing in customer service”, knowing that concerned customers would be calling.

“We’re also making sure we keep the relationship between the broker and the customer,” he said. “We’re all going to work together in partnership to support the customer but also to keep them with us as well. You want to be in their midst and give them the first, best offer we can.”

Rakhit preferred not to comment when asked about APRA’s minimum loan serviceability of 3%, but he said Bankwest remained committed to adhering to regulatory requirements and responsible lending practices and always conducted its due diligence to ensure its customers were in appropriate financial positions.

On this point, Cunliffe said ANZ offered a product called Simple Refinance, which meant that “if you’re going to lower repayments than you’re currently on, it’s a very simple verification process”.

Rakhit said Bankwest had already introduced measures to support existing customers, with options including loan term extensions and shifting to interest only for those customers with a good track record.

Nectar Mortgages’ Stephen Harris said mortgage brokers adhered to two regulations: the best interests duty and responsible lending obligations. “So, on best interests duty? Absolutely, we’re good to go. On BID you take that policy and go, ‘It’s in the best interest of the client to reduce their rate and move them’.”

But responsible lending required that brokers had to know the client and prove affordability, Harris said. “We don’t have to prove affordability on any lender’s individual calculator, but we do have to answer to ourselves and our licensees: how does the client afford the loan?”

He said brokers had to ask questions such as: Is there any indication of mortgage stress? Have they paid the loan on time for the last 12 months? Has there been any change in their income over that period?

“As long as you’re ticking all those boxes, you’re OK. But if you reach the end of the review and the client’s living expenses and income suggest they can’t afford the loan, the broker can’t write it, even if ANZ’s willing to take it.”

What’s your approach to cashbacks? Elwig said BOQ Group had enjoyed a strong year and had done well when it came to refinancing.

“The non-majors were priced competitively,” he said. “In 2023, some of the majors have now gone back into pricing, so there’s a pressure on margins for everyone now on the front book.”

When it came to cashbacks, the group had a multi-brand strategy, Elwig said. Virgin Money did not provide cashbacks, while BOQ offered cashbacks, and at ME cashbacks were based on LVRs.

He said cashbacks were “bedded in now”.

“I know that brokers want to get away from it, but it seems to be part and parcel of the market,” Elwig said.

Fedder said that for the last 12 months Suncorp Bank had refinanced more loans in than out. Under BID, brokers had been able to place Suncorp Bank and non-majors on the “top of the menu” for customers, and this was driving refinance flows, he said. The sector offered competitively priced refinancing and brand trust.

“There’s also the pro-broker element of a non-major bank,” Fedder said. “Our successes are directly linked to the broker market. I think that’s important not just to brokers but to customers as well.”

Rakhit said Bankwest had changed a lot of policies to suit refinances in the last 12 months, including valuations and credit reporting. “We’ve stripped out so much of the documentation that we once needed, and your refi customer is generally very low risk because you can see that continuity of payment.”

Referring to Elwig’s comments about cash- backs, Rakhit said it raised the question of rate versus cashback. “Margin is becoming an increasing conversation, and we’re aware that there’s loans being written beneath cost of capital,” he said.

Rakhit said brokers would remain critical to Bankwest navigating the current market, as they provided invaluable insights into what borrowers were preferring, such as cheaper rates or cashback offers, which could help shape future offerings.

Melanie Cunliffe (pictured above) from Indigo Finance questioned what kind of consumer behaviour or loyalty was being driven by cashbacks.

“Is that what we want, that everyone’s going to be chopping and changing all the time?” she said. “Some people are saying, ‘I’ll take a slightly higher rate because I’m getting a cashback, but then I’ll just go and refinance in a year or two’.

“In our business, we try to encourage our clients to get loans that are going to suit them for the longer term.”

ING was one of the last lenders to bring in cashbacks, Gibson said. Brokers are now saying, “We’re getting clawed back because customers are churning us”.

“Customers are going back to the same broker again because they feel bad and are going to different brokers for cashback,” he said.

Harris (pictured above) questioned how banks balanced the cost of cashbacks.

“What I’m hearing is you’re writing it off over seven years, but loan terms are now less than four years. Our loan terms are coming down because we continue to offer cashback,” he said. “The client’s gone; you’re not getting any more income out of that client. You’ve thrown your money away up front en masse.”

Brokers weren’t in favour of cashbacks, Harris said. “It doesn’t do us any good. It’s the unholy trinity of cashbacks, offsets and clawbacks – that’s not an environment a broker wants to be in. If you tell us that you’ve got a really good product that’s going to last for a long term, and it’s got all the right features, we will sell it – that’s BID.”

Harris agreed with Fedder on non-banks’ partnerships with brokers helping the sector to grow. “Non-majors probably have a better relationship in general with brokers than the majors.”

He said it also made sense that majors dominated the purchase market; non-majors would do better when it came to refinances. The more interesting question was whether non-majors were acquiring more new clients to market.

Gibson agreed with Harris but said there was a combination of factors helping the non-majors. One of these, in the second half of 2022, was major banks offering below-the- line pricing.

“We had a lot of feedback from brokers saying, ‘I can’t be bothered with asking for below-the-line pricing; I just know what I get with you guys [non-majors], so I’m just going to come to you’.”

Gibson said that in the past two years non-major banks had also invested a lot in process efficiencies and enhancements for refinances, trying to remove paperwork wherever possible.

Cunliffe said, “I’ve seen a huge shift in our clients’ perception of non-majors, and a huge opportunity for them. When interest rates were low, customers wanted to stick with the majors, but as rates rose and people felt the pinch, they were more open to other lenders.” Another factor pushing more clients to the non-majors was the algorithm-based retention pricing of some major banks. Cunliffe said that despite brokers speaking to retention teams, in some instances great clients were not being offered competitive retention pricing, and were even offered rates “nearly 1% outside what we can get elsewhere”.

Rakhit said Bankwest had decided a few years ago to offer back-book customers front-book pricing. This meant telling a broker that the bank would offer 4% to their customer, based on LVR and loan size.

“If you’ve got a customer that’s already with us, we will reprice to that same 4% … it’s a very easy task and all a part of our goal to be a simple, easy bank for the Australian homeowner of today and tomorrow,” Rakhit said.

In an environment in which margins were being squeezed, the question for banks was whether they wanted to focus on front-book acquisition or back-book retention.

“The past few years have been great for being able to acquire. I’m not sure it’s going to be as easy to acquire new customers in the next couple of years, in the current market of affordability challenges,” Rakhit said.

He asked the brokers for their thoughts on the loan volumes they would write over the next year.

“We absolutely think our volumes will drop, but not hugely,” Harris said. He believed there would be a lot of turnover, with brokers trying to take advantage of better loan offers for their customers.

Nectar Mortgages had pulled back on the number of loans brokers would write per month, but Harris said the business hoped to attract more brokers overall.

It was a similar situation at Indigo Finance, Cunliffe said, with the brokerage focusing on resourcing, quality service and looking after its existing clients.

Fedder said there was lot of talk in the media about headwinds to home loan system growth in the next 12 months. “I think that does lead to the importance of looking after existing customers in that environment.”

Rakhit responded by saying, “Troy said this before, but this is where I think brokers play a role that nobody else can play.”

During COVID, every customer rang their broker, and they played such an important part in helping customers with their options, Rakhit said. Bankwest’s approach was to come up with solutions it believed would fit the customer’s situation, such as an interest-only loan extension or a reprice.

“Bankwest strives to be the best bank for brokers in the country, and, in turn, brokers are critical to Bankwest, with more than 80% of our home loan customers originating from brokers,” he said.

“It’s critical in a relationship such as that to ensure brokers have the options, tools and support to hand to provide fast, easy and simple support for their customers – and that’s how we’ll get through the next 12 months.”

Rakhit said non-majors provided unique support to brokers, such as Bankwest’s case-ownership model and direct BDM support, because of that mutually collaborative relationship.

“We don’t have that large-scale distribution, we don’t have the multistorey call centres to be able to handle that volume of traffic, so our approach is always going to be different, and when it comes to brokers, that means working closer and more collaboratively.

“Brokers know our customers best,” Rakhit said. “So the broker should be able to say, ‘This is the best option for you’. We’ll partner with brokers on this.”

Elwig asked the roundtable what percentage of fixed rate maturities non-majors would be able to refinance.

Rakhit said he spoke recently to a broker who “had seven refis on his desk and not one would service”. “You’ve got to stay with your lender, and I’ve just got to try and get the best possible outcome from that lender.”

Fedder said about 9% of Suncorp Bank’s customer base were due to roll off fixed rates over calendar year 2023, and the bank was supporting these customers in a number of ways.

“About six months ago, we rolled out what we call a portfolio view of customers so brokers can see their customer base, which has had great feedback,” he said.

“We know the broker is going to have a needs-based conversation with their customer, so making sure we are there to support brokers is part of that process.”

This included making sure the bank’s pricing processes were quick, Fedder said, as well as investing in functionality to provide a much faster speed to answer.

“Suncorp Bank has invested quite significantly in our broker portal in the last two years, and that allows brokers to go to that to help support the ongoing relationship as well.” Elwig said a significant number of BOQ Group customers would be rolling off fixed rates, and they would be contacted ahead of time.

“We report all maturities data to the brokers in advance,” he said. “We also have a link straight to the portal to do retention pricing from there.”

Elwig said the group was also looking at improving portals, such as by including existing customer information and streamlining loan maintenance processes to make things easier for customers.

Gibson said that from an industry perspective, when the pandemic hit in 2020 everybody wanted to have surety on loan repayments, so three-year fixed rates became the most popular product. He said ING had started reaching out to its fixed rate customers last year, following a well-thought-out process that involved pre-emptively talking to customers about budgeting and other helpful tools.

As the time to fixed rate expiry drew nearer, the contact centre made outbound calls, talking to affected customers. Gibson said this was an important investment the bank wanted to make to ensure customers knew what interest rates they were facing, what the process involved and what options they had.

Rakhit said about 20% of Bankwest’s book would be rolling off fixed loans over the next two years. The bank had started writing to customers eight weeks out, encouraging them to call their brokers.

“This is where Bankwest’s focus on the customer ensures they are receiving the best possible support, because we would rather they ring their broker so we can begin working with them as soon as possible, and I think this is a really good opportunity for customers to further engage with the broker.”

Bankwest has invested in efficiencies that now ensure its valuation tool is dynamic, with repricing based on LVRs, which means brokers have access to up-to-date figures, and the whole automated process can be completed in 18 seconds.

Bankwest has initiated teams across its business to identify fixed rate roll-off customers in varying segments according to their financial position, and it’s now proactively providing them with loan offers.

Rakhit said a feature called Footprints was being built within the portal, which enabled the bank to see if a broker had not accepted a price for its customer. That would then inform the bank’s strategy for further options for customer retention.

“I want to try and get some feedback on any [customers] that we’re not keeping, because that’s just as valuable – if not more so – than those customers we’re retaining. Is it just price?” Rakhit said.

“We strive to be a simple, easy bank for the Australian homeowner of today and tomorrow, and we’re placing just as much of a priority on supporting existing customers as we are on attracting new customers. If we can provide the best possible experience and help customers over the next two years in the ways that suit them, acquisition is going to flow naturally.”

Cunliffe said it was interesting to hear that the non-majors were talking about renegotiating loan terms.

“How would that play with compliance?” she said. “Because if we renegotiate a client’s loan term, then we’ve actually got to go through the full process again, whereas as a bank, you don’t. How can we work together on that?”

Rakhit responded by referring to term extensions and interest-only extensions. He said it was a good industry challenge to say, “The customer is not borrowing any more money, and it’s not a hardship case”.

“How do we support them? How do we avoid this being seen as a material credit event? Is there an exception that might be possible?”

He said for some customers the only option would be a forced sale, “which is no good for the economy or the person”.

Harris said that during the pandemic customers could get a loan extension or a mortgage holiday and it didn’t affect their credit rating. “We now roll into what is probably the fallout of that. You can’t take action forever and constantly plug holes in buckets. At some point, if somebody’s overcommitted, or their circumstances have changed, there’s going to be pain, and it’s unfortunate, but it’s true.”

But there was no reason why, if interest-only was allowed back then without affecting credit rating, it shouldn’t be allowed now, Harris said. Even 40-year loan terms, as painful as they were, should be considered.

He agreed with ING’s policy of letting customers know about their fixed rate roll-offs as early as possible so they could plan for it.

“Knowledge is power,” he said. “If people aren’t looking, they’re probably going to get blindsided and hurt.”

Elwig said BOQ Group was trying to improve its loan maintenance processes and make it easier for brokers to access the data so the banks could act on it faster.

“We’re also in the process of putting the customer information on the portal so you can do your annual reviews,” he said. “We’re also planning to bring all three brands onto one platform and have it fully digitised.

“When we get to that stage, it’s not just about the acquisition; it’s about loan maintenance, using the app to do things and making it easier for a customer to do things.”

Cunliffe said her clients asked about rates they saw pop up in their bank app and whether they should accept them.

Elwig explained that with all of BOQ’s and Virgin Money’s fixed rate maturities, brokers were given 60 days’ notice via email of the new rates, and a link to the pricing tool.

Rakhit pointed to Bankwest’s history of working in close collaboration with brokers to deliver the tools and services they wanted and needed, with its investment resulting in initiatives such as the recent DocBox document upload tool.

He welcomed feedback from brokers on what the next enhancement could be to the intuitive Bankwest Broker Portal, which launched in 2018.

“We’re constantly speaking with our critical broker network, and we have some exciting plans in the pipeline, but we’re also an open door, and I encourage brokers to let us know any pain points they want or need addressed, whether they believe it’s critical or just a nice-to-have,” Rakhit said.

Gibson agreed that broker feedback was important. “If there’s a need or desire or want, we’ll make it happen,” he said. “I really encourage any broker to give us feedback, because we listen, and we will do something about it.”

Lenders all have marketing and lobbying departments. Are they being used to protect brokers, and in turn themselves?

Gibson said he was well aware of the details. “It impacts everybody, real estate agents,

franchisees, franchise networks, banks … we understand that this is not just an aggregator issue, it’s a sub-aggregator and broker issue. We’re trying to assist in any way we can.

“From a non-major perspective, we have a very strong industry. We are absolutely supportive of our brokers and anything that impacts our industry.”

Gibson said ING worked with industry bodies to help educate decision-makers on how the issue affected the broker industry.

Fedder added that non-major banks had sought to really understand the issue, and the consultation across the industry had been outstanding. “I think the MFAA in particular has done a great job in communicating and rallying the industry.”

A united industry voice can help generate good outcomes, Fedder said.

Rakhit said Bankwest’s focus was on deliv- ering the best possible experience for brokers so they in turn could deliver the best possible experience for customers.

The Bankwest Broker Portal was central to that commitment, and Rakhit said the bank was focused on investing in areas that created efficiencies for brokers through automation, self-service and support, freeing up time that brokers could then invest in customers.

Rakhit said Bankwest’s focus on ‘speed to yes’ had resulted in upgrades to its valuation tool, while its use of consumer credit reporting data reduced the document burden on brokers. “We think we can take that one or two steps further now on income and potentially then even use optical character recognition,” he said, referring to an automated process that could identify information from a payslip, for example, without a colleague needing to review it.

“We think we can put more tools in the broker’s armoury, making their job and their experience with Bankwest simpler and easier and giving them the confidence that Bankwest can get to yes quicker, ensuring they can deliver the best possible experience to their client and, potentially, retain them long-term.”

Fedder said Suncorp Bank had also invested a lot in its speed to approval.

“When I look at Connective’s turnaround time report, we’d be the equal or number one lender for turnaround times now,” he said. “The investment has been in tech; we’ve invested a lot into the NextGen platform.”

Suncorp Bank’s entire loan assessment process right through to unconditional approval used NextGen technology, halving turnaround times for unconditional approval, Fedder said.

BOQ Group was also looking to improve its time to yes, Elwig said. Catch-up compliance tabs had been implemented for BOQ and Virgin Money to make it easier to reduce NYRs. “We’ve also introduced NextGen ID for non-face-to-face, to make that easier. In April, we’re looking at introducing DocuSign for the customer application forms,” he said.

“In a year’s time, we’ll be rolling out a more efficient process; time to yes will be a lot quicker with better digital documents and therefore workflow. It’s all more automated.” At ING, Gibson said it was all about getting out of the broker’s way and reducing the time brokers spent on getting a loan deal approved. “We’re all focused on time to yes,” he said. “We’re going to develop automated processes and our use of data to improve turnaround times.