Jump to winners | Jump to methodology

MPA reveals Australia’s top-ranked aggregators for 2026, as voted by more than 720 experienced brokers across 11 service categories in the industry’s long-running annual survey,

from commissions to technology and lending-panel quality

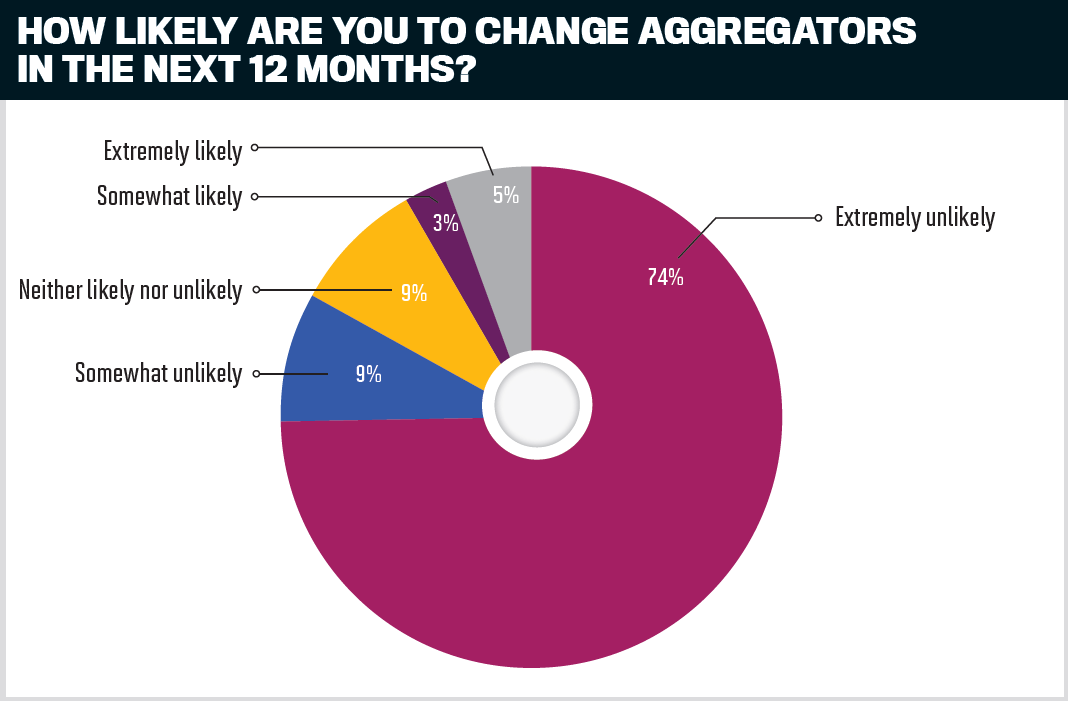

There is a version of loyalty in the mortgage broking channel that looks, from the outside, a lot like contentment. Three-quarters of brokers say they are extremely unlikely to switch aggregators. The same three services have topped the priority list for five consecutive years. Satisfaction with the fundamentals remains solid. On paper, the aggregator model has never been more entrenched.

But look at where the numbers have moved. Brokers’ reluctance to switch aggregators has fallen from 81% in 2023 to 74.75% in 2026, and the brokers crossing into ambivalence are not new entrants still finding their footing. They are experienced operators. Most have been in the industry for over a decade. Nearly one in three settles more than $40 million annually. When brokers at that level start hedging, the question worth asking is not whether they are about to leave. It’s what they are no longer certain about.

The answer, repeated across thousands of responses in MPA’s 16th annual Brokers on Aggregators survey, is this: the aggregator model was built to process loans; broker businesses have evolved to advise, retain and grow client portfolios.

“Most aggregators are still built around a transactional model,” said brokers from Victoria, NSW and Queensland. “Modern broker businesses are increasingly relationship-driven, advice-led and portfolio-focused. The real value sits in client retention, ongoing reviews and strategic structuring, not just settling a loan.”

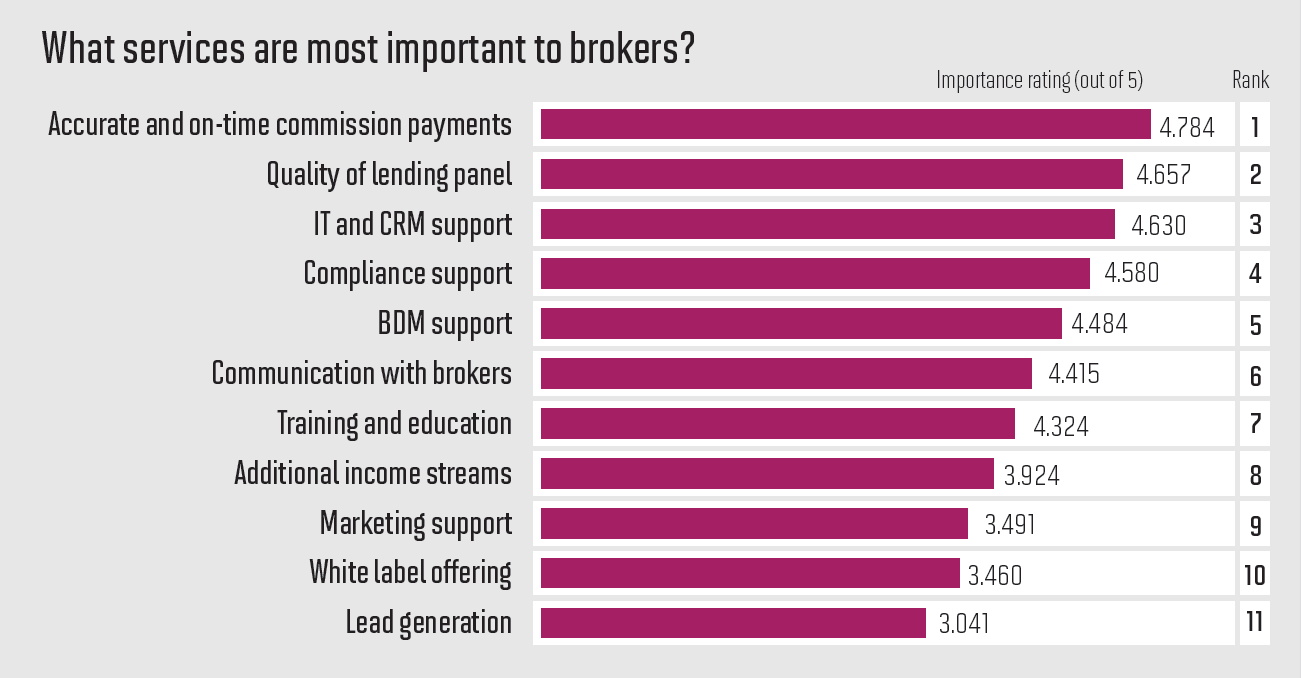

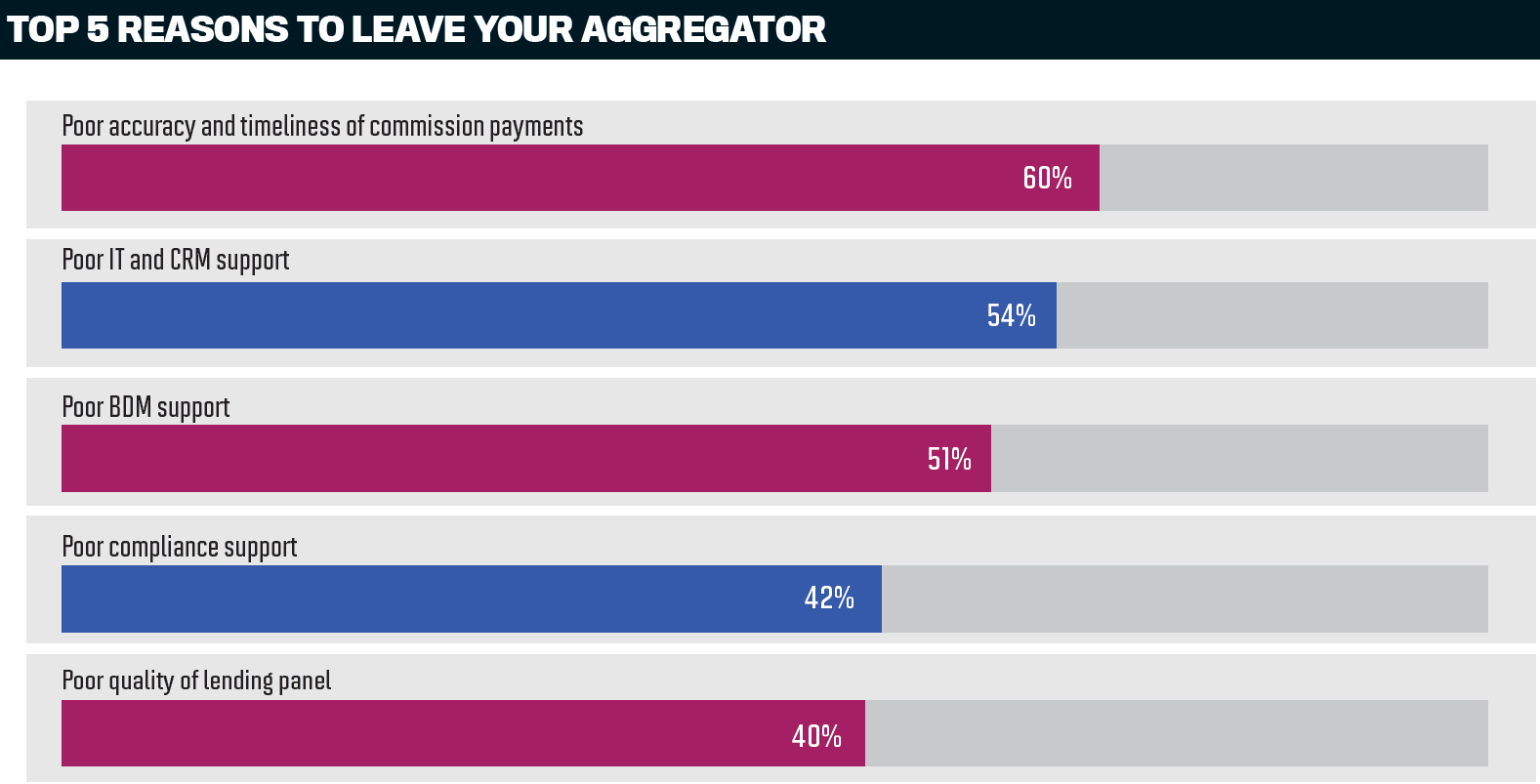

The data makes the pressure points precise. When asked what would make them leave, 60% of brokers nominated poor commission accuracy, 54% poor IT and CRM support and 51% poor BDM support. All three have held those positions since 2023.

Mathew Rehayem, head of white label and strategic partnerships at non-bank lender Pepper Money ANZ, puts the commercial consequence in no uncertain terms. “It’s no longer about scale alone. It’s about relevance, speed and helping brokers win more deals in an increasingly competitive market. Aggregators are becoming a genuine growth engine, backing brokers with real capability, stronger support and partnerships that help brokers grow, rather than simply providing access to lenders.”

One broker frames what comes next: “The next wave of growth will come from better tools, better data and better client-facing experiences.”

The aggregators recognised in this report are the ones already delivering that. MFAA data shows brokers facilitated 81% of all new residential home loans in the March 2026 quarter, driving $124.88 billion in settlements, up 25.7% year on year. The channel’s ambitions run higher still. Rankings are based on broker scores across 11 service categories, each rated out of five, with a minimum 10% network response rate required for inclusion.

Brokers tightened the brief on commissions, lending-panel and technology in 2026, and the aggregators that delivered are breaking from the field

The rankings of what brokers value most look unchanged. The scores underneath them are not. Commission accuracy has fallen from 4.811 in 2023 to 4.784 in 2026. Lending-panel has dropped from 4.689 to 4.657 and IT and CRM from 4.668 to 4.630. The order hasn’t shifted. The grading has grown harder.

The bottom of the table tells the same story in reverse. Lead generation sits at 3.041 in 2026, down from 3.093 in 2023. White label has fallen to 3.460 from 3.596. Marketing support is at 3.491, down from 3.727. The gap between top and bottom has widened. Brokers are raising the bar where it counts and grading everything else accordingly.

The aggregators earning the highest marks understand what that means in practice. Justine Harris, Nectar Mortgages head licensee and finance specialist in Kellyville, NSW, describes what best-in-class commission support actually looks like.

For a high-performing brokerage, accurate and timely commission processing impacts staffing decisions, cash-flow management, confidence in reporting, business planning and even customer service.

“The best aggregator relationships are the ones where brokers don’t have to think about commissions because the systems and support behind the scenes are reliable and transparent,” says Harris.

Gippsland Finance Solutions director Jaime Savory, who settles approximately 1,200 loans annually, keeps one member of her 20-strong team dedicated solely to tracking commissions. “If I don’t get my commission payments on time, I can’t pay wages,” she says.

When asked what would make them leave their aggregator, 60% of brokers nominated poor commission accuracy, 54% poor IT and CRM support and 51% poor BDM support. All three have held those positions since 2023.

Beyond the structured responses, open-ended broker comments pointed to cost as the dominant theme, specifically fees rising without corresponding service improvement. Autonomy surfaced across multiple responses, with brokers citing restrictions on how they interact with clients and, in some cases, tension between aggregator commercial interests and broker independence.

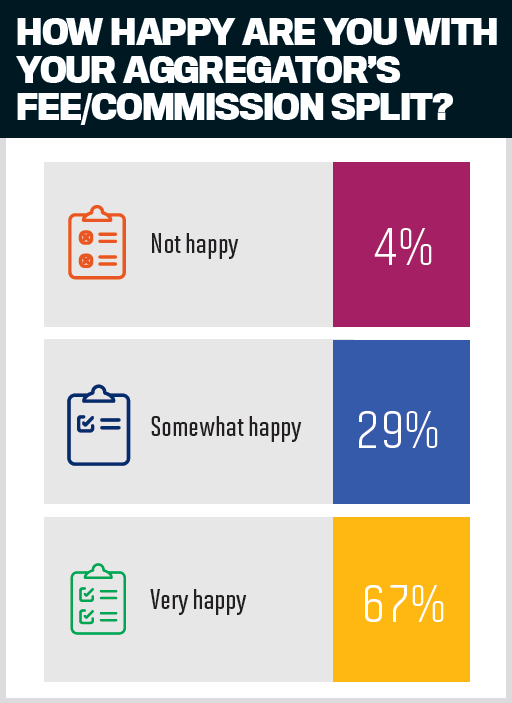

Overall fee and commission-split satisfaction remains broadly positive, with 66.43% of brokers reporting they are very happy and 4.37% not happy. For many, the flat-fee model is the reason.

Lending-panel quality held second place for the fourth consecutive year at 4.657. Harris measures panel strength by coverage across customer types, policy niches and servicing models. “The stronger the panel, the more confidence a broker has in solving complexity.”

Savory reinforces the point from a volume perspective. Five or six years ago, smaller lenders barely registered. Not any more. “Nowadays you need a variety of lenders that you can offer different solutions for different clients.”

The most common broker request was for more non-bank and niche lenders for self-employed, alt-doc and complex scenarios.

IT and CRM support ranks third at 4.630. Brokers rating their aggregators highest on technology keep coming back to the same thing: the system saves time and stays out of the way.

National Mortgage Brokers took gold for commission accuracy, AFG silver and outsource Financial bronze, separated by less than a tenth of a point. Outsource Financial led IT and CRM support, ahead of AFG and Connective. Loan Market led lending-panel quality, with outsource Financial taking silver and AFG bronze.

Among boutique aggregators, MoneyQuest led all three top-ranked categories. Liberty Network Services took silver for commission accuracy and IT and CRM, and bronze for lending-panel. Purple Circle took silver for lending-panel, and bronze for commissions and IT and CRM.

ACCURATE AND ON-TIME COMMISSION PAYMENTS

Aggregators

National Mortgage Brokers

AFG (Australian

Finance Group)

outsource

Financial

Boutique aggregators

MoneyQuest

Liberty

Network

Services

Purple Circle

Financial

Services

ADDITIONAL INCOME STREAMS

Aggregators

outsource

Financial

National

Mortgage

Brokers

AFG

(Australian

Finance Group)

Boutique aggregators

MoneyQuest

Liberty

Network

Services

Purple Circle

Financial

Services

IT AND CRM SUPPORT

Aggregators

outsource

Financial

AFG (Australian

Finance Group)

Connective

Boutique aggregators

MoneyQuest

Liberty

Network

Services

Purple Circle

Financial

Services

QUALITY OF LENDING PANEL

Aggregators

Loan Market

outsource Financial

AFG (Australian

Finance Group)

Boutique aggregators

MoneyQuest

Purple Circle

Financial

Services

Liberty

Network

Services

COMPLIANCE SUPPORT

Aggregators

outsource

Financial

National

Mortgage

Brokers

Loan Market

Boutique aggregators

MoneyQuest

Liberty

Network

Services

Purple Circle

Financial

Services

WHITE LABEL OFFERING

Aggregators

AFG (Australian

Finance Group)

Connective

Finsure

Boutique aggregators

MoneyQuest

Purple Circle

Financial

Services

Liberty

Network

Services

From clawbacks to AI and rising fees, brokers spell out exactly what they need aggregators to do next

Broker frustration comes into sharp focus in the 2026 survey feedback. The themes that surface most consistently are not about aggregators failing at their core functions. They are about aggregators not evolving fast enough beyond those functions.

Pepper Money ANZ’s Rehayem says brokers don’t need more process. They need lenders and aggregators who help them say yes to more customers.

“Real partnership comes from working closely with brokers to co-create solutions, from policy settings through to technology enhancements, based on what’s happening in market,” he explains. “Ultimately, innovation should deliver real outcomes for brokers and clients alike, including faster decisions, smarter matching and fewer dead ends throughout the application process.”

Technology is where the gap is most visible

Nectar Mortgages’ Harris identifies technology as the point where aggregator performance most clearly diverges. The highest-performing aggregators don’t have the longest feature list. They are the ones where technology works reliably, integrates well into workflow and creates efficiency gains across customer communication, compliance, lead tracking and post-settlement engagement.

“When systems are clunky or disconnected, brokers end up duplicating work, manually tracking information or relying on workaround processes,” Harris says. “That becomes a major scalability issue.” Brokers increasingly value aggregators willing to evolve their technology ecosystem over time rather than treating CRM as a static platform.

Brokers’ wish-list items make the same point in operational terms: AI integrated into CRM workflows, better automation of compliance and fact-finding, and seamless connectivity between lodgement platforms and lender policy tools.

“An AI admin assistant that can create all the documents, handle compliance, get emails ready, [do] more of the heavy lifting with all the back end prior to lodging of the application” was one broker’s wish.

Another described a specific proactive tool: “An automated, AI-driven equity tracking and repricing alert system would shift the broker from a transactional role to a proactive adviser, protecting their trail book from churn.”

A third asked for something simpler but equally telling: “A post-settlement portal that provides clients’ loan details, current rate, fixed rate expiry, original LVR. This would help provide ongoing service and new deal opportunities.”

Rehayem names the underlying problem. “The biggest gap is often between access and execution,” he says. “Brokers have more lender options than ever before, but what they really need is speed, clarity and confidence in knowing where and how a deal can get done.”

Fees are rising. Perceived value is not keeping pace

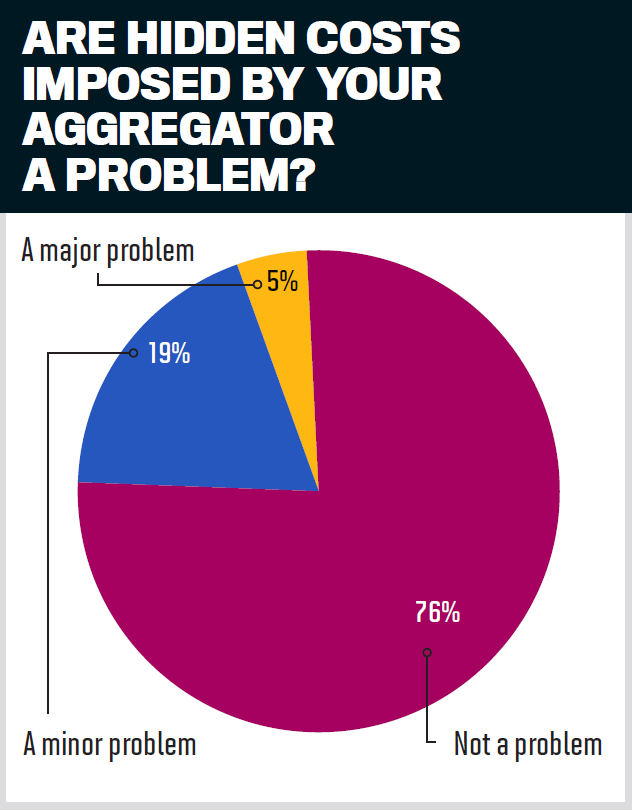

Hidden costs register as a major problem for 4.65% of brokers and a minor problem for 18.76%. Brokers’ frustration is about the direction in which some fees are going.

“Less fees. They are charging a lot but also cutting service with the use of AI, which should make it more affordable or provide better service. It doesn’t feel like that,” one broker said.

Another was more precise: “The services offered are fine. It’s the cost imposed by the aggregator for those services, many of which we don’t use.” A third described a creeping pattern: “They are giving us back services that were already included in our fee instead of changing the parameters and charging for a service that was originally free.”

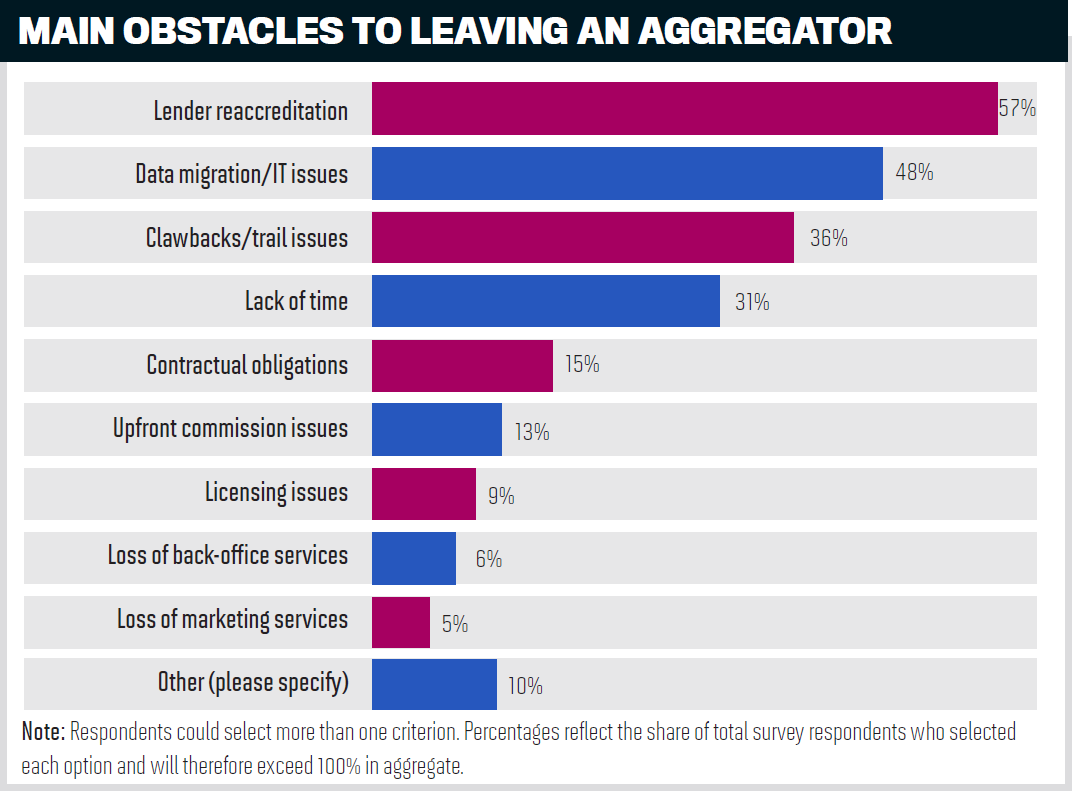

The clawback issue continues to generate sharp responses. “They could be much more active in getting changes to clawback,” one broker said. The sense across multiple responses is that aggregators have the industry relationships to push harder on clawbacks but have not done so with sufficient urgency.

The services brokers are building towards

Lead generation remains the lowest-rated service at 3.041. “Lead generation is time-consuming, and the aggregator could create a pretty good funnel on scale for a shared fee,” one broker said. Another described it as the single biggest hurdle in their business.

Commercial and diversification support surfaced as a gap for brokers who have moved beyond residential. One said, “I need specialists in commercial and agri lending. I receive no support due to what my business does.”

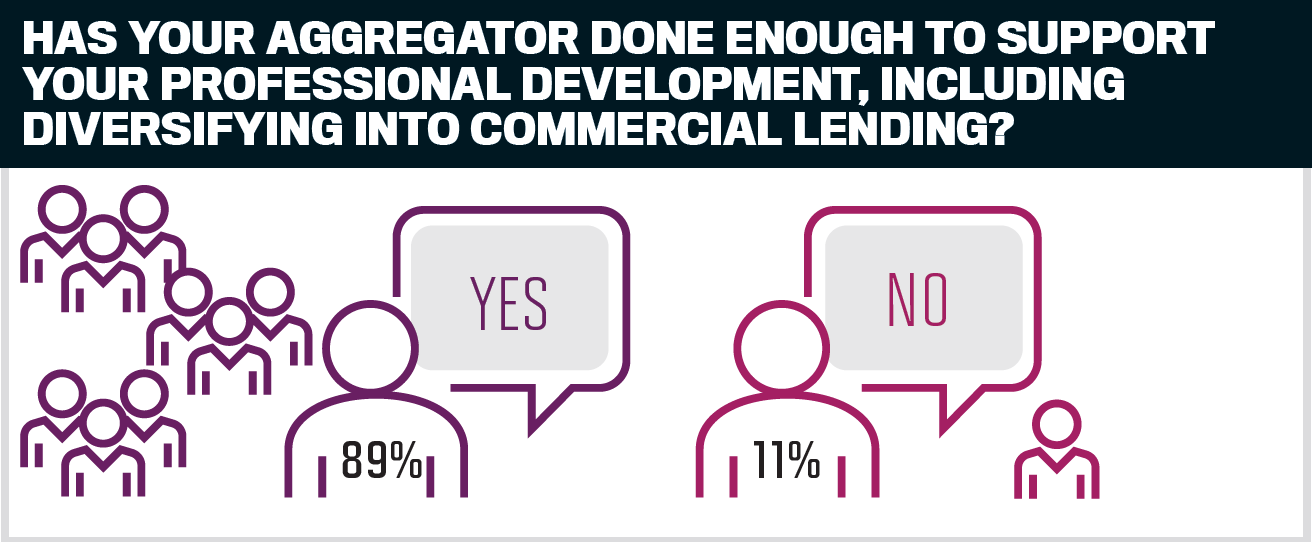

Professional development satisfaction is broadly strong at 88.70%, but exit planning is a notable gap. “I find with all industry organisations they focus a lot on new broker education but not a lot on brokers looking to exit in the next five years. It would be nice to have more training on how to increase the value of your trail in preparation for sale.”

The referral opportunity sitting in plain sight

Gippsland Finance Solutions’ Savory identifies a gap that no one in the industry appears to have yet closed. Every home loan and refinance requires an insurance certificate. Brokers hold the client relationship at exactly the moment insurance decisions are made.

“You’ve got a first-home buyer who you’ve held the hand of the whole way. And now we say, ‘Go and find your insurance. Good luck’.” Savory would like to see aggregators move into that space, giving brokers an insurance referral pathway within the same group.

“Every home loan, every refinance, everything we do we need to provide an insurance certificate for, but we don’t have anyone that can help us do it. For me, that is the biggest gap,” said one broker.

The 2026 rankings reflect what happens when an aggregator treats broker needs as a brief, not a complaint.

Among aggregators with more than 600 brokers, outsource Financial delivered a dominant overall performance, claiming gold and leading eight of 11 service categories. The result ends Loan Market’s reign at the top of the 600-plus rankings. AFG took silver overall with gold in one category, four silvers and five bronzes, the most consistent podium presence in the tier. Connective secured bronze overall.

In the boutique category, overall gold medallist MoneyQuest swept all 11 service categories for the second consecutive year, a clean sheet no aggregator in either tier matched. Purple Circle Financial Services, which held overall gold in 2025, took silver. Liberty Network Services claimed bronze, finishing second across seven categories, including commissions, additional income streams, BDM support, compliance, IT and CRM, lead generation and marketing.

The aggregators brokers trust most have mastered the fundamentals. Getting the basics right is the price of entry. What brokers are asking for now is something harder to deliver and easier to ignore.

LEAD GENERATION

Aggregators

outsource

Financial

AFG (Australian

Finance Group)

National Mortgage Brokers

Boutique aggregators

MoneyQuest

Liberty

Network

Services

Purple Circle

Financial

Services

MARKETING SUPPORT

Aggregators

outsource

Financial

National

Mortgage

Brokers

AFG (Australian

Finance Group)

Boutique aggregators

MoneyQuest

Liberty

Network

Services

Purple Circle

Financial

Services

COMMUNICATION WITH BROKERS

Aggregators

outsource Financial

National Mortgage Brokers

AFG (Australian

Finance Group)

Boutique aggregators

MoneyQuest

Purple Circle

Financial

Services

Liberty

Network

Services

BDM SUPPORT

Aggregators

outsource Financial

National

Mortgage Brokers

AFG (Australian

Finance Group)

Boutique aggregators

MoneyQuest

Liberty

Network

Services

Purple Circle

Financial

Services

TRAINING AND EDUCATION

Aggregators

outsource Financial

AFG (Australian

Finance Group)

National

Mortgage Brokers

Boutique aggregators

MoneyQuest

Purple Circle

Financial

Services

Liberty

Network

Services

As broker businesses evolve beyond loan processing into advice, technology and client retention, MPA asked whether their aggregators are keeping pace

MPA presents the final ranking of Australia’s top aggregators and boutique aggregators in 2026 based on brokers’ votes across 11 award categories

In MPA’s 16th annual Brokers on Aggregators survey, brokers were asked to rank their aggregators across 11 categories: accurate and on-time commission payments; IT and CRM support; quality of lending-panel; communication with brokers; BDM support; compliance support; training and education; additional income streams; marketing support; white label offering; and lead generation. Brokers could rank their aggregator with a score out of five in each category.

Due to the varying sizes of aggregator groups and disparities in the number of respondents, only those that achieved a response rate of at least 10% from their broker network were included in the final list.

MPA also asked brokers an additional question about their aggregator’s service and support, which did not impact the overall score.