The FHA's fees have more than doubled since the bust and now with more relaxed lending standards in effect, homeowners could save up to $12,000 with PMI, according to WalletHub data.

The new Fannie Mae and Freddie Mac mortgage guidelines that were announced Monday may make it easier for prospective home buyers to qualify for loans, but it may also shake up the mortgage insurance market.

The new rules resulted from an agreement in October meant to clarify when lenders would be penalized for making mistakes on mortgages they sell to the mortgage giants. The guidelines lower the minimum down payment from 5% to 3%.

Relaxing lending standards could make it possible for hundreds of thousands of additional consumers to get mortgages. They should also provide some flexibility when it comes to down payments, something that disappeared after the crisis.

After 2008, many mortgage insurance companies went out of business because of the massive amount of loan defaults. Thus, the private mortgage insurance (PMI) companies that did survive became pickier about borrowers they would cover.

Government-insured loans soon became the top option for borrowers who couldn’t make the 20% down payment. Federal Housing Administration (FHA) volume has more than tripled from 2007 to 2009.

FHA fees also skyrocketed. The annual insurance premium paid by most FHA borrowers has risen to 1.35%, up from 0.55% in 2010 — or more than $300 a month on a $300,000 mortgage. The higher premiums helped beef up the agency’s cash cushion when its finances took a hit after the housing bust.

The jump has equated to homeowners with FHA loans paying $17,398 in premiums during the first five years after the purchase of a median-price home ($212,100), compared to just $9,210 in 2008, according to personal finance website WalletHub.

The website analyzed the new FHA rules and has concluded that a home buyer could save up to $12,000 with PMI compared to FHA. “Consumers with down payments below 20% can save $2,251 - $12,026 in just five years by choosing private mortgage insurance instead of an FHA loan,” according to report. However, the savings depends on the borrower’s credit score and down payment.

While an FHA loan requires a mortgage insurance payment for the life of the loan, PMI does not. With a low down payment conventional loan, homeowners may be able to stop PMI payments once they achieve at least 22% equity in the property -- reducing monthly mortgage payments by more than $100, the report stated.

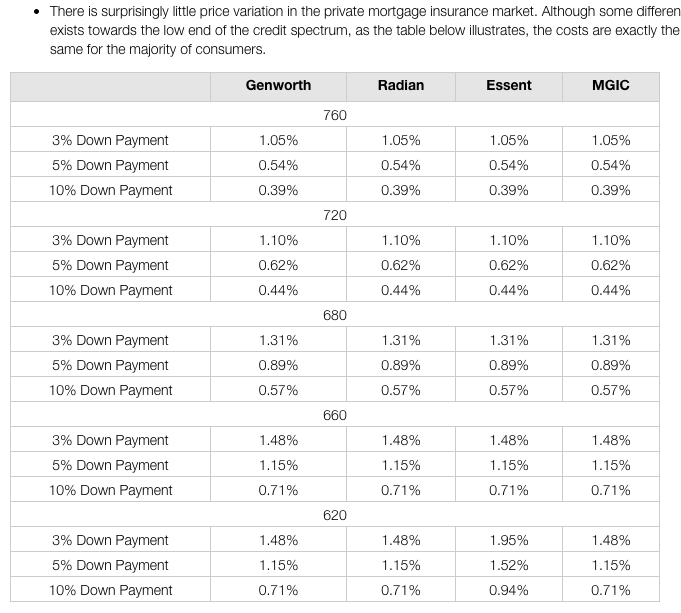

There is also surprisingly little price variation in the private mortgage insurance market. Although some difference exists towards the low end of the credit spectrum, as the table below (click to enlarge) illustrates, the costs are exactly the same among Genworth, Radian, Essent and MGIC.