A combination of Australia’s ageing population and high property prices is driving up demand for reverse mortgages. MPA and Heartland Seniors Finance explain how brokers can get started

.JPG)

A combination of Australia’s ageing population and high property prices is driving up demand for reverse mortgages. MPA and Heartland Seniors Finance explain how brokers can get started

Downsizing homes has become a catch-all solution to Australia’s housing affordability problems. Consequently, a significant part of the federal budget was devoted to reducing barriers to downsizing by allowing superannuation contributions from the sale of homes. Yet there are plenty of reasons why senior Australians don’t want to downsize, ranging from the pensions assets test to stamp duty and the desire to grow old in familiar surroundings.

It’s for these reasons that an increasing number of borrowers are turning to reverse mortgages. Reverse mortgages unlock equity from the home without requiring repayments, and do not allow the borrower to owe more than the value of their home. The borrower repays the loan inclusive of accrued interest when they pass away, move out, or sell the property.

It’s for these reasons that an increasing number of borrowers are turning to reverse mortgages. Reverse mortgages unlock equity from the home without requiring repayments, and do not allow the borrower to owe more than the value of their home. The borrower repays the loan inclusive of accrued interest when they pass away, move out, or sell the property.

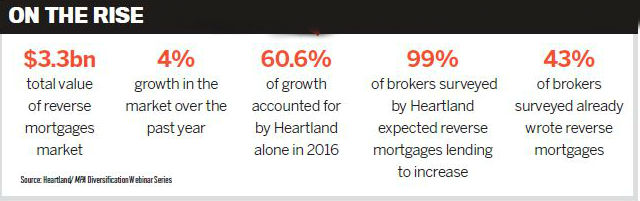

Heartland Seniors Finance has offered reverse mortgages since 2004, but recently it has seen a surge in awareness of this type of loan, according to CEO Andrew Ford. “The increasing indebtedness you read about in the media is affecting the average loan size we see, and an increasing number of applications are for refinance, with much larger loans than we saw historically.”

“We’ve grown very strongly and we’re expecting that to continue,” Ford adds.

He explains that while Australia’s ageing population will naturally create more reverse mortgage clients, the political landscape is accelerating this process, with demands for increased means testing of pensions against valuable property creating asset-rich but cash-poor clients in capital cities. These clients will need funds to retire on, accessed through reverse mortgages.

A broker’s role

A broker’s role

You need a credit licence to write a reverse mortgage, giving brokers an instant advantage over accountants and financial planners. Brokers also have an edge over the few banks left in this space, argues Heartland’s head of distribution Craig McInnes. “The broker offers something the clients value very much; that is the in-home service: going round and having a cup of tea and a scone with the clients and talking about their deal.”

Start by looking at your existing network. Ford recalls one broker who wrote letters to clients he’d dealt with 10–15 years ago. A few of those clients were now aged over 60, thus eligible for a reverse mortgage, and several took him up on the offer. Alternatively, Ford says, “a lot of our enquiries come from the children of prospective borrowers, but it might be networks of accountants and financial planners as well as increasing enquiries online”.

The borrower profile affects the loan: in Heartland’s case the maximum LVR starts at 15% and increases with age in yearly increments to 45% for those aged above 90. A maximum of two borrowers is allowed (additional occupiers are permitted) and the LVR is set at the age of the youngest borrower.

Residential properties in all capital cities and many regional centres are eligible, covering 97% of the country by population. Heartland also offers reverse mortgages on investment and holiday home properties. Repayments and redraws are available, with the amount being available as a lump sum, regular advance or reserve drawdown.

There’s no maximum loan size. Heartland has written up to $1.8m, but according to McInnes “we’re open to bigger loans if you’ve got them”.

Whether or not Heartland appears on the panel, most brokers are able to write reverse mortgages after a short accreditation process. “Not every broker writes every product,” says McInnes. “What we have found is that people who step into the reverse space find that it’s easy; it’s straightforward; you’re dealing with great clients; they stay in it. We rarely deal with people who write one loan and disappear.”

Loans typically take around four weeks, says McInnes, with potential bottlenecks being the valuation and the need for the client to consult their solicitor as part of the process. Brokers then receive upfront and trail commission or, if they prefer, upfront commission only. Although trail is paid, reverse mortgages can be an easy option for brokers, McInnes explains. “Once the loan is written there’s not much ongoing maintenance involved; they do a last a lot longer than your average home loan.”

Crest of the wave

Heartland CEO Ford sees demand for reverse mortgages only moving in one direction. “This is the beginning of a wave that’s really going to pick up as we overcome some barriers around awareness and apathy.”

Those barriers are diminishing: ASIC’s MoneySmart website now has an extensive section on reverse mortgages, and Heartland produces a range of blogs and YouTube videos on the subject that are raising awareness.

The biggest push factor, however, may be necessity, as a generation of Australians struggles with life on the pension.

“The pension covers the essentials but nothing really else,” Ford says. “For people that need more, accessing the equity in their home can be transformational.”