Born between 1980 and 1995, Millennials are one of the largest and demographically diverse generations in U.S. history.

By Rajesh Bhat

Special to MPA

Born between 1980 and 1995, Millennials are one of the largest and demographically diverse generations in U.S. history. Their financial decision-making and purchase behaviors are distinctly different than preceding generations, perhaps because they have grown up with the Internet and mobile phones, have lived through a significant economic recession during their prime working years, and are more educated than their predecessors.

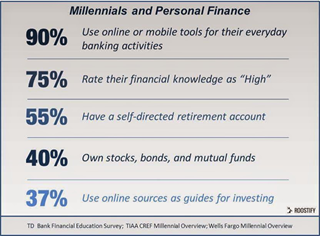

As Millennials assume a greater share of labor markets and the consumer market, businesses in every industry are eager to understand this demographic in order to shape their strategy, and their attitudes and actions related to personal finances play a major role in the analysis. One of the main characteristics of this generation is that they are online and very hands-on when it comes to personal finances.

Millennials feel empowered to make day-to-day decisions in their personal finances. This confidence leads to greater optimism about their ability to assume debts; in fact, 80% of them have at least one source of long-term debt and more than half of them manage large debts as soon as they leave college. This confidence and optimism extends into the home-buying and mortgage space.

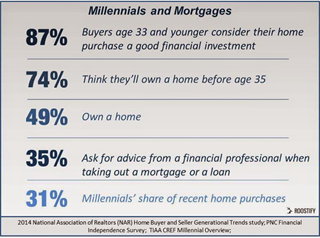

Millennials and Mortgages

In the area of home buying and financing, Millennials are reinforcing the behavioral themes of gravitating towards mobility, speed, and convenience that they demonstrate in other verticals. And as the table below indicates, they are also exhibiting optimism and ambition when it comes to home ownership.

For many Millennials, home purchase is more than the American dream - it is an expectation, a financial milestone towards which they aspire and manage. As they become more hands-on with their own personal finances they also feel empowered to make a decision on mortgages with less professional assistance than previous generations.

Rajesh Bhat, CEO

When, as a management consultant, Rajesh Bhat bought his first house in the Bay Area, the process was a nightmare because of the lack of visibility into the loan and other parts of the transaction. He founded Roostify to streamline the process and make it easier for lenders, buyers and agents to interact and create a more efficient way of securing a loan and purchasing a home.